Their names are in our history books: James, Dillinger, Cassidy, Bonnie, Clyde … The bank robbers of lore.

Their stories, triumphs and demises have been sewn into the fabric of our country and we have romanticized them in film and tv for decades. During their runs, most of us even rooted for them to get away. They were our Robin Hoods.

Their portrayal wasn’t always accurate, however.

Some of these celebrated criminals, like Bonnie and Clyde Barrow, were actually brutal and savage killers. Others, like John Dillinger and Butch Cassidy, rarely resorted to violence at all and really were the respected, noble men we believed them to be.

No matter their method or madness, these sack filling bandits baffled police chiefs, filled headlines, and were bigger-than-life celebrities of their time.

But, this phenomenon was short lived. In only a few decades, outlaws went from being household names to afterthoughts on back pages.

Like they did so many times, their reign (from the late 1800s to the early 20th century) disappeared quickly and inconspicuously.

We didn’t just stop caring, bank robberies also became less frequent. After their viral wave of the early 20th century, bank robberies in the U.S. slowed down to almost a complete halt by the mid-1960s (when less than a thousand banks were robbed a year). Likewise, murder, rape, theft and other forms of major crime also declined during these golden years.

Bank robbery and other crimes soon mounted a comeback, though. As an unintended result of stunted population growth following WWII, Baby Boomers were getting to the prime crime committing ages (between 15 and 25 years old) and all crime went up.

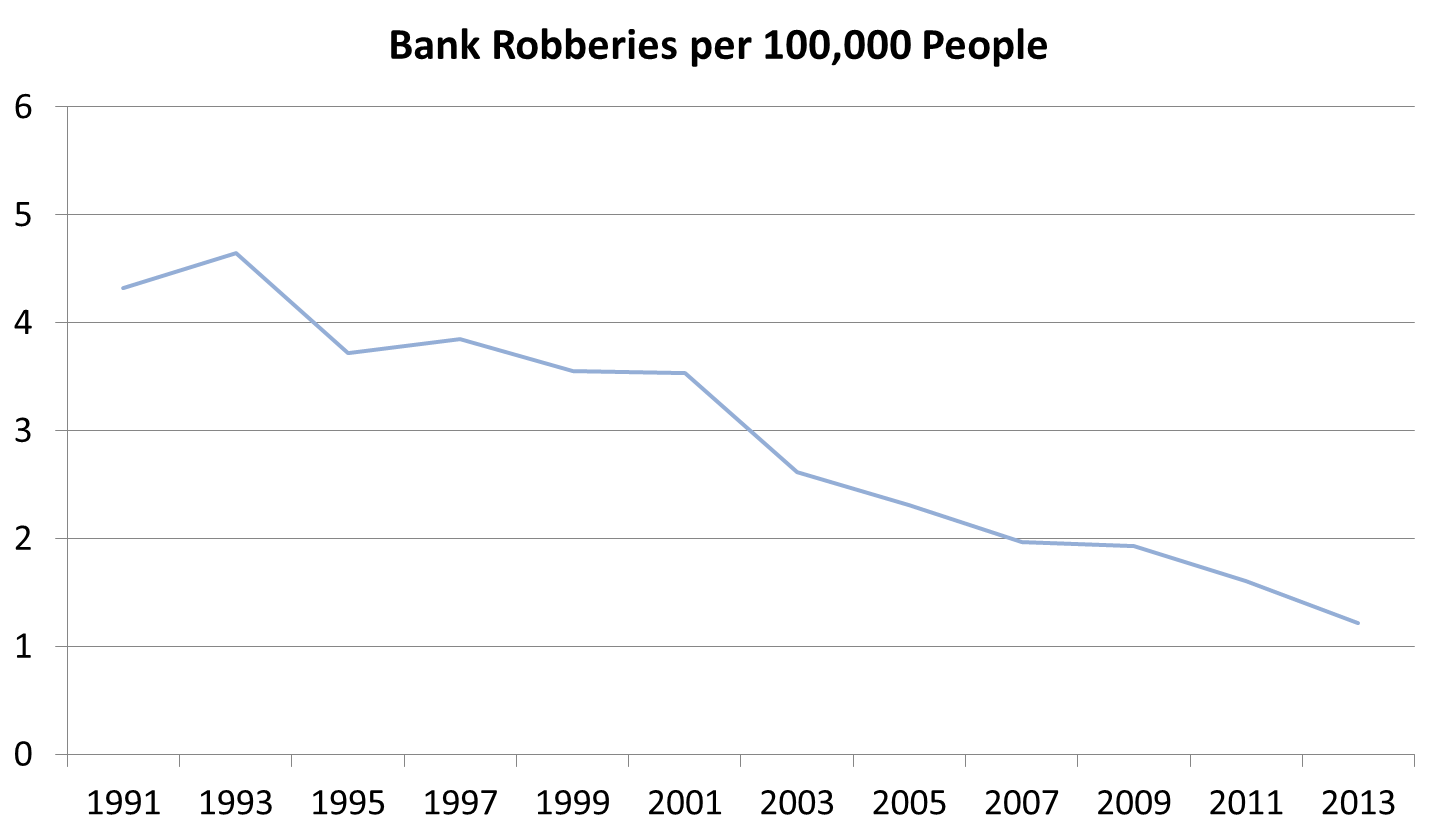

This climb in rates continued to an all-time high of 12,000 bank jobs in 1993. These years – during the early 90s – were the worst crime years in American history and nearly every form was at all-time high rates.

Then, peculiar things started happening with bank robberies in relation to these other major crimes…

Just after 1993, the number of murders, rapes and thefts plummeted in the United States. Bank robberies, on-the-other-hand, remained pretty stagnant for the next 10 years or so. There was not a comparable drop in bank robberies (like with other crime) until 2003, when murders, rapes and theft all flat-lined again.

Here is how the trends compare…

At first glance, these two trends look pretty similar; they both peak around the same time and ultimately decline. What interested me, though, was the difference in timing and rate of their declinations.

Murder rates reduced dramatically from 1993 to 1998, when, in 5 years the rate was cut in half. This timing and rate of decline is similar to almost every other form of major crime in the U.S. (besides bank robberies).

Bank robberies did not start significantly declining until a decade later — around 2002-2003. It also took much longer (almost 10 years), for the same 50% reduction experienced by other forms of major crime. It seemed to be declining for reasons other than population shifts. It was declining more naturally.

Stranger still, the numbers show that bank robberies are continuing to decline. The other forms of major crime have all stayed relatively constant after their drops, but not bank robberies.

Do the odd trends and independent declines mean that they are going away completely?

It just might.

Here are a couple of reasons people generally point to as why they may be going away:

The easy and generally accepted explanation is technology improvement. That, ATM machines, security cameras, and anti-theft devices are making it harder to steal money. I’m not sure I completely buy this explanation, though. Criminals have always stayed neck-and-neck with technology and the ratio of successful to failed bank robbery attempts has been pretty constant for the last 30 years or so. Additionally, the percentage of recovered stolen dollars hasn’t really changed at all; meaning that we aren’t any better at catching the successful robbers later . People are just as likely to get away with robbing a bank today as they ever have been.

Another explanation is that banks don’t take physical deposits nearly as much. The argument is that they aren’t getting actual dollars in the door any more and everything is online. This is true, but what they are required to keep hasn’t really changed in 100 years (other than inflationary adjustments). What is available for the taking at banks now is about the same as it was for Dillinger, James and Cassidy.

You may now be thinking, “Isn’t this a good thing, though? Shouldn’t we hope bank robberies become a thing of the past?”

No. We shouldn’t…

The reason why we shouldn’t is also the same reason why bank robberies may very well be going away — and it’s not because of security measures or online deposits. Let’s not pat ourselves on the back just yet.

The reason is that there now is a huge difference between dollars and money.

Dollars are physical pieces of currency that you can hold and look at. Dollars are what trade hands and sit in bank vaults.

Bank robbers steal dollars, not money.

Much more “money” exists in the world than dollars, and money is entering circulation at a much higher rate. In fact, out of the entire money supply, only around 3% is currently in tangible, dollar bill form. This percentage will only continue to decline.

Simultaneously, inflation is rising and the cost of everything is going up. In 1915, a gallon of milk cost $0.13, a bag of sugar was $0.30, etc. (this is a well known and widely accepted result of inflation, you’ve heard all of these numbers hundreds of times). Every day something is more expensive than it was the day before.

Thus, the physical dollar is not very economical to steal in today’s world. Dollars are not only representing a smaller portion of the total money supply but everything is costing more of them. 100 years ago, when John Dillinger stuck up a bank and demanded $50,000 cash, he could do a lot more with that loot than he could today. The amount of dollars that John can stuff in a sack wouldn’t get him very far anymore.

Remember when banks were huge buildings made of concrete, brick and mortar?

They used to look like temples and gave off the appearance of security. Some, even had actual vaults, where cash from deposits were kept.

What do banks look like today?

They are thrown up with the same cheap materials as any fast food restaurant or convenience store. Most new banks are even smaller in size than your typical McDonald’s or 7/11 (and often less fortified).

Banks, at this point, are begging robbers to steal from them. The truth is, banks really wouldn’t care if they did. I mean, robbers could only take what little cash they did have and the value of that cash is declining anyways.

“But, wait a minute … In part 1, you said that dollars are printed out of debt. And because of this, cash doesn’t have any real value at all. How can we devalue something that already doesn’t have value? That’s mathematically impossible, isn’t it? No matter what you divide zero by, the result is still zero.”

Well, that’s correct. You cannot devalue something that doesn’t have any value to begin with, yet the dollar seems to be devaluing.

What’s actually happening is an increase in the value of debt. Remember, debt makes dollars. In order for the dollars to seem legitimate, debt has to seem legitimate.

It’s just simple slight-of-hand … Cash is made out of debt because debt is not tangible. But, debt has no value of its own. So, in order for cash to seem like it has value, debt has to seem like it has value.

“How does one just give something value?”

Well … that’s where it becomes a bit more challenging. And it takes time. But it can be done…

1) Allow people to pay for things with it.

2) Create multiple avenues to access it.

3) Provide incentive for using it.

These same concepts gave precious metals their value when they were the standard for our currency:

1) Things could be paid for with gold.

2) Dollars used to be redeemable in gold, so those who weren’t prospectors could still access it.

3) Gold was traded on markets and even given a rating by agencies like S&P.

The difference is that when the standard of money is something like gold, the standard is still tangible. Debt is not.

So, what was once intangible and valueless, became very real and extremely precious: debt.

1) Debt started circulating. Suddenly, we were given the ability to redeem things directly with debt (a check then a credit card) and new debt engines went into circulation from there, i.e. mortgages, stock trades, escrow, student loans, online payments, etc.

2) Debt is also pretty easy for anyone to access. Although a bit more restricted now, financial institutions have been handing out high limit credit cards for years. As recent as a decade ago, a $500,000 home on an annual salary of $60k was no problem. All of the sudden, debt let us buy things we could never afford.

3) Finally, the advantages of using debt are everywhere. From alcohol to medicine and happiness to war, America has been flooded with a barrage of advertisements enticing us to spend. They really don’t even try to hide it anymore and debt itself is advertised. MasterCard told you it was “Priceless”, Chase says it gives you “Freedom”, and Visa creepily says it’s “Everywhere You Want to Be” (Visa is probably the only honest one). For our most frequent debt shoppers, we hand out credit card points, air miles, and refinancing options.

The result is a very unique sense of need in America. We feel like we need things that no one else in history has ever needed. We need things to be new and different so badly that we are fine with buying a new cell phone every year or a car every three. This insatiable need has even created new ailments: “shopaholic”, obesity, sex-addiction all entered our lexicon and are common illnesses. All the while the amount of “money” goes up, making these needs cost so much that we can no longer pay for them with cash. We have to pay for them with debt.

Thus, debt and money are taking cash completely out of the equation.

But it’s all just a trick, an illusion of cash losing value through an illusion of debt gaining value, and tricks only work if you want to believe they’re real.

We constantly reaffirm our belief with every swipe of the card.

“But what does this mean? Besides, of course, robbers no longer finding a bank hit worth it.”

It means that our system allows for banks to increase and regulate the entire money supply (that is created out of debt) and increase and regulate the entire debt supply (that is created out of money).

They are now masters of the universe.

“Then … Where is all this money?”

It’s nowhere, really.

Money is like a hot potato. It’s lent out as soon as it is received. The person or entity that receives that loan then deposits it, and it’s lent out again by their bank. Where it is deposited and lent. Deposited and lent. And the process continues (theoretically) forever. All the while earning interest for the lender at each stop.

Even if robbers did want to steal money from banks today, most of it would be gone before they even they even walked through the door. What they could actually get their hands on isn’t worth the risk any more.

But … if the bank robbers ever figured out a way to access our money (instead of just stuffing their bags with cash) then we would all be in big, big trouble…

That’s why I wish bank robbers would still practice their craft. That’s why I miss Dillinger, Cassidy, and even Bonnie and Clyde. I’m alright with bank robbers stealing dollars … as long as that keeps them away from the money.

At least then we could find some comfort in knowing their take wasn’t worth very much.